Welcome to our support page! We want to ensure that your experience with our club management software is smooth and hassle-free. Whether you have a question about how to use a feature of QuikChek Cloud, or need assistance troubleshooting an issue. We are ready to assist you every step of the way. Alternatively, you can browse the QuikChek Cloud Help Page for steps, or reach out to us directly through our support line (954) 575-7160 / option 2. Your satisfaction is our top priority, and we’re committed to resolving any concerns you may have promptly and efficiently.

How to download files: Left click on a download link, and you will be prompted to save the file to your computer.

QuikChek Cloud Cheat Sheet 06.20.18

{kind=link}

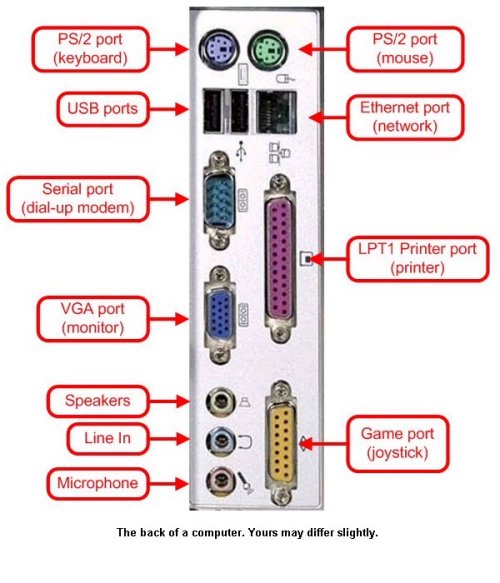

System Requirements for QuikCheK

***For those purchasing new computers***

We recommend Dell computers with Windows 10.

For monitors we recommend a 20″ flat panel.

| Recommended System Requirements – Windows 10 – 3.0+ Ghz Processor – 8 GB RAM min (16 GB RAM recommended) – 20 ” wide screen monitor – Sound card with speakers (For Check-In) – An Uninterruptable Power Supply for ALL QuikCheK stations – USB 3.0 ports (for peripherals, scanners, printers) – Any inkjet or laser Printer – A DSL, LTE or Cable Internet connection – 20″ wide screen monitor – 500 GB Hard drive or higher – Sound card with speakers (For Check-In) – 24x CD-Rom drive – A high speed internet connection.Supported Operating Systems (mobile devices) -Android 5.0 or higher and iOS 10.5 or higher (only for using the application, data input and viewing on the browser not for using hardware such as barcode scanner)Unsupported Operating Systems: -Windows 8 -Windows 7 Starter Edition -Windows Vista Home -Windows XP -Windows 2000 -Windows 98/SE -Windows ME -Linux -AmigaOS -Do not use All-in-One computers Door Controller System Requirements – Serial PortReceipt Printer – We recommend a USB thermal receipt printer. Please click here.Browser – We recommend using the latest versions of Google Chrome, Mozilla Firefox, or Apple Safari in order to ensure the best user experience.Servers – You do not need a server, the application is accessed via the internetOther Specs – Microsoft Office or Open Office for printing mail merge letters. Coral Springs Software highly recommends Dell Computers (they’re the best!) Power Outages Recommended Anti-Virus Software |

01 Refer to issuer

This is when the cardholder’s issuing bank (Visa, Mastercard, Discover, American Express, etc.) blocks the transaction.What to do: First and foremost, always apologize. Even if it isn’t your fault, you can demonstrate empathy and compassion to customers. In the case of an 01 error code, ask for a different card. If the customer doesn’t have one, have them call their credit card company to investigate and resolve the issue. There’s usually a toll-free number somewhere on the card.

02 Refer to issuer (special condition)

This is similar to 01 Refer to issuer in that the cardholder’s issuing bank blocks the transaction from going through.What to do: The same guidelines apply to 02 as they do for 01 — ask for a different payment method or have them call their card issuer. If the latter happens in a retail setting, direct them to a comfortable area of your store while they address the problem. Never say anything about their declined card loudly enough for other customers to hear.

04 Hold-call or Pick up card

Again, this credit card declined code is when the issuing bank blocks the transaction, typically because of a suspected issue. Issues could include a lost/misplaced card, expiration, or fraud, among other red flags.What to do: Though uncomfortable, this code indicates that the merchant must seize the credit card. There’s typically a toll-free number somewhere on the card that you or an associate can call to get direction on next steps.

05 Do not honor

Again, this credit card declined code is when the issuing bank blocks the transaction, typically because of a suspected issue. Issues could include a lost/misplaced card, expiration, or fraud, among other red flags.What to do: Though uncomfortable, this code indicates that the merchant must seize the credit card. There’s typically a toll-free number somewhere on the card that you or an associate can call to get direction on next steps.

07 Hold-call or Pick up card (special condition)

Again, the cardholder’s issuing bank is stopping the transaction. However, this time it’s because of suspected fraud.What to do: Don’t accept any form of payment from this customer. You might also take the card and discreetly call the toll-free number, somewhere out of sight and earshot of the customer in question and throughout the store.

12 Invalid transaction

This time, the error might be happening on the merchant side of things. A 12 credit card decline code indicates that the transaction is invalid. You might have entered information or dollar amounts incorrectly or even pressed a wrong button.What to do: Check and/or reenter all the billing and purchase information you entered. If there are no issues, start from the beginning.

13 Invalid amount

Here, the error is definitely on the merchant end, and it’s because the dollar amount was invalid. It might be negative for a purchase, or positive for a refund. Or you could have accidentally included a letter or symbol.What to do: Fix the dollar amount and try again.

14 Invalid card number

Similar to error 13, 14 pins down where the problem lies. You likely mistyped the credit card number.What to do: Carefully reenter the credit card number.

15 No such issuer

Credit card declined code 15 gets even more specific, alerting the merchant that the entered credit card number doesn’t start with an appropriate number:American Express: 3

Discover: 6

Mastercard: 5

Visa: 4

What to do: Check the first number entered in the credit card information and adjust as needed.

19 Re-enter

Now we venture into unknown territory. Here, your payment processor is telling you it doesn’t know what happened and why it didn’t work.What to do: Attempt the transaction again. If it still doesn’t work, the merchant or customer may have to call the issuing bank. Give the customer the option in this scenario.

25 POS condition code invalid value

25 is typically similar to 14 or 15 — essentially, there’s something wrong with the credit card and billing information.What to do: Again, carefully reenter the information or retry the transaction.

28 File is temporarily unavailable

In this scenario, there was a blip during the authorization process, which is the initial part of the transaction.What to do: These errors are typically temporary, so simply waiting a bit and retrying the transaction should work. If it doesn’t, you’ll want to contact the issuing bank or your merchant account provider.

41 Hold call, Pick up card (fraud account)

Here, the issuing bank is blocking the transaction because the cardholder has reported it as lost or stolen. Therefore, it’s essentially “frozen” for use.What to do: This is a suspected case of fraud, so you’ll have to call the toll-free number and report the incident to the issuing bank. Prudent merchants may choose to deny serving these shoppers. Or you can request an alternative form of payment — ideally cash.

43 Lost/stolen card, Pick up (fraud account)

Again, we have a suspected case of fraud because the cardholder has reported the card as missing or stolen.What to do: Just like with code 41, you’ll need to report the incident and probably opt for cash payment.

51 Insufficient funds

Transaction errors occur when the cardholder has reached or exceeded their credit limit amount. In some cases, your purchase would be what puts them over the edge — for example, if they’ve spent $4,995 with a $5,000 limit, they won’t be able to make a $5.01 purchase from your business.What to do: Similar to most other cases, you’ll want to apologize for the inconvenience before requesting an alternative form of payment. They can also choose to call their credit card company to try and sort it out or increase their limit.

54 Expired card

This credit card declined code indicates that the expiration date entered has already passed, meaning the card is expired and no longer valid for issuing payment.What to do: First make sure you entered the expiration date correctly, and if so, you can request an alternative form of payment from the customer.

57 Transaction not permitted – card

Code 57 means the credit card isn’t properly configured for the transaction you’re trying to process.What to do: Provide transaction details to your customer and have them call the bank to request permission for the transaction.

58 Transaction not permitted – terminal

These errors are with your merchant processing account, indicating that it’s not configured to process this transaction.What to do: Reach out to your merchant account provider rep or support team for further assistance reconfiguring your account.

61 Exceeds issuer withdrawal limit

Again, we have an issue where the cardholder may have overspent or withdrawn too many funds from their associated account.What to do: Request alternative payment or a customer call to the issuing bank.

62 Invalid service code, restricted

Some merchants choose not to accept American Express and/or Discover cards because of high fees and chargeback rates. If a customer attempts to pay with an unaccepted card, you might see this credit card declined code. Another cause for code 62 is if an online shopper is attempting to make a payment with a card that isn’t compatible with online payments.What to do: In the first case, you’ll need to apologize and ask for a different form of payment. Some customers may be unhappy to hear your choice, so it’s important to come up with a prepared response to express your empathy and reasoning. In the case of the latter, you’ll want to implement an error message that asks customers to use a different card or call their bank, citing the error code.

63 Card is restricted or security violation

If your credit card reader has a hard time reading the three- or four-digit CVV or CID (card identification) code, you’ll see this declined code. The CVV and CID can be found either on the front or the back of the card (depending on Visa, AmEx, etc.)What to do: Usually you can just try the transaction again without including the code. If you do this, give your customer a heads up because their bank may flag the transaction as fraudulent.

65 Activity limit exceeded or insufficient funds

Here, your customer might have exceeded their credit limit or hit their maximum number of transactions for a specific period of time.What to do: Like in many other scenarios, ask for an alternative form of payment or recommend they reach out to their credit card company.

78 No account, no such account exists, invalid account, or nonexistent account

There could be a number of reasons why this credit card declined code shows up. It essentially boils down to the bank not recognizing the account — maybe it’s no longer active, for example.What to do: Ask for a different payment method. In this scenario, it’s probably better for the customer to call their credit card company after they leave your place of business.

85 OR 00 Issuer system unavailable or no reason to decline

This credit card declined code is not as serious, as it indicates a temporary communication error.What to do: Try the transaction again. If you repeatedly have trouble, reach out to your payment processor.

91 Issuer or switch is unavailable

This is another communication error, this time concerning the authorization communication.What to do: Again, there’s no real reason this happens, so you can typically just try it again.

93 Violation, cannot complete

This indicates some sort of issue with your customer’s credit card account. The issuing bank blocks these transactions.What to do: Ask for a different payment method or recommend they contact their bank.

96 System malfunction / system error

When you see this error code, your technology may have failed you — but usually only temporarily.What to do: Simply re-administer the transaction after a few minutes. If it’s still a no-go, contact your payment processor directly. They may have you instruct the customer to call their bank as well.

97 Invalid CVV

This credit card declined code is also descriptive. It means the CVV is wrong. The CVV is the Card Verification Value and is typically three digits and found on the back of the card, though American Express has four-digit CVV codes on the front of the card. This is an extra security and verification layer to help prevent fraud.What to do: Double-check you’ve entered the CVV correctly. Some cards might have multiple three- and four-digit codes, making it hard to decipher which one to use. If you get an error message again, try one of the other codes.